Helium's HIP 149 and the Realignment of Helium's Deployer Economics

1. The Network passes HIP 149

Our initial Helium case study asked whether the network's token value was tied to real revenue or to a subsidized rate propping up the illusion of one. Helium's own governance just answered that question. HIP 149 cuts the carrier-paid rate from the $0.50 per gigabyte Nova had been subsidizing down to $0.10, the rate carriers will actually pay at scale, and retires Proof-of-Coverage entirely in favor of rewards tied to usage. Helium moves from a bootstrap-phase incentive, paying hotspots to exist and be available, to a maturity-phase incentive, paying them for data they actually deliver, now that most Mobile deployments reach carrier offload within weeks of going live. IoT sees a smaller version of the same shift. PoC retires there too, but IoT deployer income was already pegged to data credits, so the change is narrower in practice.

In place of Proof-of-Coverage, Mobile deployers now earn through a two-sided reward band, a minimum tied to carrier revenue and a cap that redirects excess upside to veHNT stakers. The proposal also mints roughly 141 million HNT over three years into an operations and growth vault, with a seven-seat Advisory Council overseeing that spending. The gap between hype and fundamentals the original case study flagged before the data existed to prove it has now closed, on-chain, in public, through a vote.

2. Why This HIP Exists - Volume Grew. Pay Didn't.

Helium's original Mobile emissions design set a target earn rate of $0.50 per gigabyte under HIP 53. That target has compressed materially at the hotspot level over the past year. Network rewardable bytes grew roughly fourfold, from about 24,000 GB per day in June 2025 to about 97,000 GB per day in April 2026, while HNT issuance stayed fixed under the HIP 20 schedule and HNT's price more than halved over the same period. The result is a widening gap between what the network was designed to pay deployers and what they actually earn in USD terms.

HIP 149 identified three problems that follow from this gap:

Deployer earnings were unanchored to the revenue the network actually generates.

Carrier-paid burn enters circulation as data credits and leaves permanently on use, with no direct link back to what carriers were paying.

Proof-of-Coverage rewarded existing infrastructure rather than active usage.

That design suited the network's early bootstrap phase, but it is increasingly disconnected from where value is created now that most Mobile deployments reach carrier offload within weeks. Operations and growth are funded year to year, with no encoded runway for carrier expansion, deployer programs, or core engineering.

These three problems shape the proposal which:

Ties deployer earnings to the carrier-paid rate keeps the burn and mint model intact while making it responsive to what the network actually earns rather than a static target set years earlier.

Capitalize operations on a bounded, self-terminating schedule replaces annual governance uncertainty with an encoded runway.

Retires Proof-of-Coverage completes a shift that HIP 147 had already begun in September 2025, when it introduced "data eats first" prioritization ahead of coverage-based rewards.

3. What Changes: The Four Bundled Decisions

One veHNT vote approves four initiatives together:

Decision 1: Deployer floor tied to carrier-paid burn rate (with the formula and the pre-vote burn rate cut from $0.50/GB to ~$0.10/GB under HIP 143)

Decision 2: Operations and growth capitalization (~141M HNT over 36 months, front-loaded)

Decision 3: PoC retirement on Mobile and IoT

Decision 4: Seven-seat Advisory Council with oversight and termination-vote authority over the capitalization

4. Deployer Impact

Deployers gain a two-sided reward band layered on top of the existing pro-rata data payout. Each epoch, baseline earnings in dollars per gigabyte are compared against the payer rate Nova sets under HIP 143. A target minimum holds deployers at no less than half that rate. An earnings cap holds them at no more than three times that rate. Between those two bounds, deployers earn the pro-rata baseline directly, with no adjustment in either direction.

Below the minimum, the protocol re-emits HNT to bring earnings up to the target. This is the mechanism worth explaining carefully, since it is more conservative than it first appears. The top-up is bounded by recently burned HNT, mostly the HNT Nova burns creating data credits for carrier offload. The protocol cannot mint more than that recent burn amount, so on its own this mechanism does not expand net HNT supply. During a sharp price drop, the burn average takes one to two weeks to catch up, so deployers may receive a partial top-up briefly before the full target resumes.

Above the cap, deployers do not keep the excess. Once HNT price appreciation pushes earnings past three times the payer rate, the surplus is redirected to veHNT stakers rather than paid out further to deployers. Total emissions do not change when the cap binds. The redirect is simply a different destination for the same HNT.

IoT deployers see no change to their income mechanism. Data transfer continues on the existing dollar per data credit peg that has governed IoT rewards since launch. What IoT deployers lose is the Proof-of-Coverage reward category itself, which retires alongside Mobile's.

The net effect for Mobile deployers is participation in both directions rather than a one-way floor. They are protected from carrier rate declines and HNT price weakness down to half the payer rate, and they share directly in HNT price appreciation up to three times that rate, with the ceiling functioning as a shared upside rather than a hard cap that simply stops paying. IoT deployers gain neither side of this and simply lose PoC, which makes IoT the network's more exposed segment under this proposal rather than Mobile.

5. Supply and Dilution Analysis

HIP 149 changes what effective max supply means for HNT. Current circulating HNT sits at roughly 182.5 million. Today's effective ceiling under the HIP 20 schedule, after cumulative reductions since 2020, sits at roughly 206 million. HIP 149 adds a third figure on top of that ceiling: the roughly 141 million HNT operations and growth supplement, minted into a vault administered by the Receiving Entity, currently Nova Labs. Combined, effective max HNT supply rises from approximately 206 million to approximately 347 million.

This supplement is a source of dilution in this proposal. It draws from neither the HIP 20 schedule nor its halvings. It has its own boundaries instead, a 12 month flat mint window followed by a 24 month linear taper to zero, both hardcoded at deploy and self terminating without requiring a future vote.

In contrast, Decision 1's target minimum mechanism, the top up that protects Mobile deployers when earnings fall below half the payer rate, is bounded rather than open ended. The top up is capped at recently burned HNT, mostly the HNT Nova burns creating data credits for carrier offload. The protocol cannot mint more through this mechanism than has recently been destroyed. On its own, this target minimum does not grow net HNT supply, and HNT supply dynamics remain long term deflationary when HNT price is low. The dilution question in this proposal is concentrated entirely in the 141 million supplement.

The tables below translate this supply picture into an implied HNT price, so the dilution figures above can be read against what the market would need to believe for HNT to reach a given level. Each table fixes a time horizon, 12, 24, or 36 months from an estimated mint start, and shows implied price across a grid of revenue growth rates and earnings multiples.

| Growth \ Multiple | 7.5x | 10x | 12.5x | 15x | 17.5x | 20x |

|---|

HNT trades near $0.24 today. At the 12-month horizon, the 20 percent growth path reaches current spot near a 15x multiple, while the 100 percent growth path clears it already at 7.5x and reaches roughly $0.53 at the top of the grid. By month 36, the 20 percent growth path reaches current spot at a lower multiple, near 12.5x, while the 100 percent growth path clears roughly $1.65 at the top of the grid.

These figures already account for the additional HNT the target minimum mints whenever price falls below the roughly $0.33 threshold where the floor binds, which is why they sit modestly below what the growth and multiple assumptions alone would imply, on the order of 2% to 5% depending on the scenario. The supplement is therefore neither dilutive nor accretive on its own. It is dilutive at low growth and low multiples and accretive at high growth and high multiples, with the crossover sitting close to where growth and pricing already stand today, and the 36-month table carries the most weight for this proposal since it spans the full life of the mint and shows the widest spread between its bear and bull corners.

6. Governance Structure Change

HIP 149 makes one clean structural cut and pairs it with a new standing oversight body. Proof-of-Coverage does not shrink under this proposal. It ends entirely on both networks, and does so on activation, when the program upgrade ships upon the Council being seated, rather than at some later phase-in. Removing an entire reward category is a larger governance step than a typical parameter adjustment, since it eliminates the verifier logic and the associated HIPs outright rather than tuning their weights.

The proposal creates the Advisory Council specifically to oversee what replaces the funding that PoC removal and the broader restructuring make possible: the roughly 141 million HNT operations and growth supplement. The Council has seven seats, five nominated by the community and confirmed through veHNT weighted voting, two appointed directly by Nova. All seven carry equal voting weight regardless of how they were seated. The Council holds NDA level information rights over how the supplement is used, including insight into the carrier negotiations that inform the HIP 143 payer rate, and can demand disclosure, publish dissent, or recommend course correction on a lower quorum of four of seven, including at least two community seats. Escalating to a full community curtailment vote, which can reduce, pause, or halt the supplement, requires a higher quorum of five of seven, including at least three community seats. Nova's two appointed seats cannot trigger or block that escalation alone.

The Council's authority is advisory and escalation based rather than a direct on chain lever. It cannot halt the supplement itself. Any actual pause or termination still requires a community voted program upgrade, and the deployer target and cap parameters in Decision 1 sit outside the Council's scope entirely.

Acceptance of the supplement also binds the Receiving Entity, currently Nova Labs, to a separate set of commitments referred to as the Receiving Entity Agreement: good faith monetization practices, a non-compete, alignment with DC burn, and long-term alignment generally, enforceable through the Council's escalation path rather than through a unilateral on chain mechanism.

Taken together, this signals a specific shift in Nova's relationship to protocol governance rather than a reduction in Nova's role. Nova remains the administrator of the vault, the setter of the payer rate under HIP 143, and the holder of two Council seats. What changes is that Nova's use of a large, front loaded funding stream is now subject to a standing, partially community controlled check with real escalation authority, even though that check cannot act unilaterally on chain. The proposal expands Nova's operational funding while simultaneously creating the first standing governance body with visibility into how Nova spends it.

7. Risks and Open Questions

Governance risk: Voters approved a governance body whose full nomination and reporting rules are still being finalized after passage rather than fixed in the vote itself, which means the actual strength of the Council's oversight over a 141 million HNT supplement depends partly on decisions made after the vote has already closed.

Deployer mechanism risk. Decision 1 protects Mobile deployers with a target minimum and an earnings cap, both tied to the payer rate Nova sets under HIP 143. The top up that funds the target minimum is bounded by recently burned HNT, so it cannot mint beyond what has already been destroyed, and the mechanism is built to preserve deflationary pressure on net supply when HNT price is low. It is also worth being direct about what the bound does and does not solve. The protocol is still printing new HNT to deliver a nominal payout target, even when that printing nets against burn rather than adding to supply on a standalone basis. A deployer receiving a top up is being paid in newly issued tokens during exactly the conditions that make new issuance least welcome to existing holders.

Whether this functions as real protection depends on what happens to that HNT once deployers receive it. If deployers hold it, the mechanism delivers on its intent. If a meaningful share sells into the market to realize the dollar value the target is meant to represent, that selling adds pressure at the same moment the price is already under strain, regardless of whether the supply math nets out over a longer window. The one to two week delay in delivery after a sharp price drop compounds this, since deployers are most exposed to a shortfall exactly when the market is least able to absorb new selling. The target minimum's actual effectiveness cannot be assessed from the supply bound alone. It depends on deployer behavior once the HNT is in hand, which is not something this proposal or its success metrics currently measure.

Deployment risk. Proof-of-Coverage paid all hotspots on the same coverage-based formula regardless of whether real usage existed at that location. This made it impossible to distinguish, under the old system, a hotspot in a high demand area from one with no sensor traffic or subscriber offload. Both earned comparably as long as they met the coverage and beaconing requirements. HIP 149 removes that requirement and replaces it with one tied directly to usage, which means the demand gap that PoC had been masking becomes visible in the reward outcome for the first time. On IoT, this shows up most clearly in rural deployments and dense hotspot clusters that earned steady PoC rewards without any LoRaWAN sensor ever routing data through them. On Mobile, it shows up in placements optimized for coverage scoring and hex density metrics that fed the PoC formula, independent of whether the location saw real subscriber traffic. The long list of anti-gaming HIPs retired under HIP 149 exists because operators found ways to score well on that formula without corresponding usage, which is itself evidence of how far the reward category had separated from demand. Locations with genuine usage transition cleanly to the new model. Locations without it see rewards drop toward zero, not because their operators behaved differently, but because PoC never required the thing the new formula now requires. The network will have to decide whether these hotspots represent latent future demand worth supporting through the transition, or infrastructure the network no longer needs.

8. What to Watch

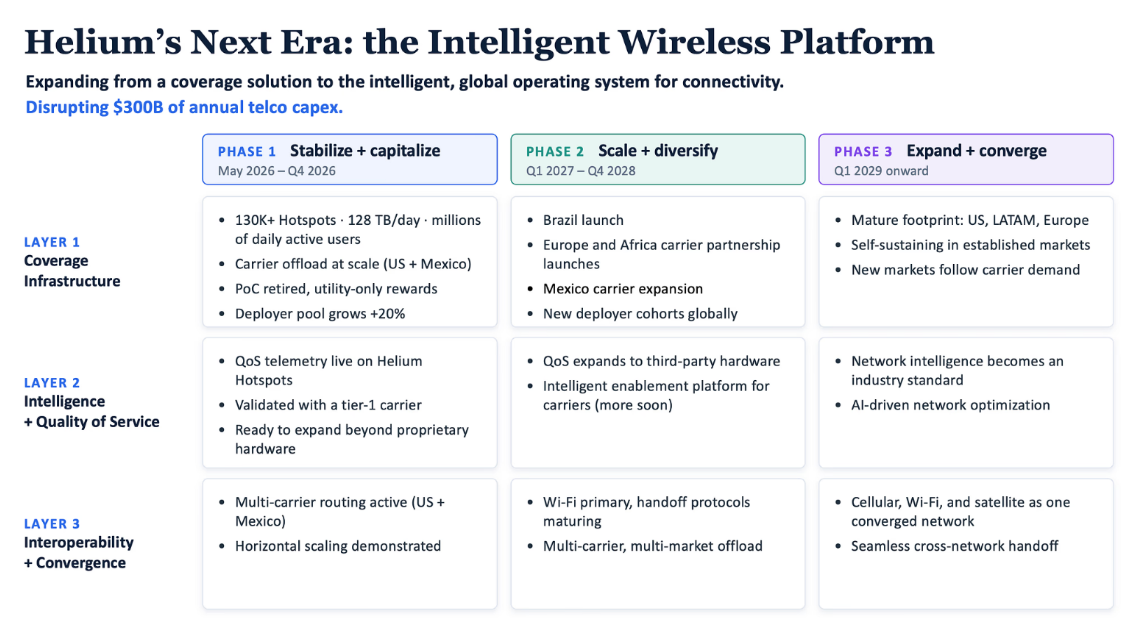

Nova's roadmap (below) frames the network's next phase in three windows: stabilize and capitalize through Q4 2026, scale and diversify through 2028, and expand and converge from 2029 onward. Phase 1's stated markers, PoC retired, carrier offload scaled in the US and Mexico, and QoS telemetry validated with a tier one carrier, are the near term checkpoints to track.

Based on an estimated Council seating by late summer 2026, the flat 12-month mint likely begins in mid-August or mid-September 2026, roughly six weeks to two months after HIP 149's July 2nd approval. On that estimate, the flat window spans the final months of the roadmap's Phase 1 and most of Phase 2, Scale and Diversify, rather than aligning with Phase 1 alone. This estimate should be revised once Nova announces an actual seating date.

The target minimum is already the binding protection for Mobile deployers. HNT trades below the roughly $0.33 threshold where the floor activates, so it will be live from the first epoch of the mint once minting starts. Carrier offload volume, measured in rewardable gigabytes per day, is the key demand side indicator against the supplement's spending.

The Council's first quarterly disclosure of vault outflows is the first real test of whether spending follows Decision 2's use of funds categories, since the Council's only enforcement path is escalation to a community vote. Longer horizon phases, international expansion, third-party hardware, and cross-network convergence, sit well past the supplemental minting taper's endpoint and carry more execution risk than anything checkable now.

Disclaimer

This case study is for informational and educational purposes only. It does not constitute investment, financial, legal, or trading advice. Nothing in this piece is a recommendation to buy, sell, or hold HNT or any other digital asset. Token markets are volatile and speculative. Conduct independent research and consult a qualified financial or legal professional before making any investment decision.

The analysis, projections, and sensitivity models in this piece reflect assumptions clearly stated throughout the text. Actual outcomes may differ materially from any scenario presented. GridEcon does not guarantee the accuracy, completeness, or timeliness of any figure derived from third-party sources, including Dune Analytics, GitHub, and other public data.

Conflicts of Interest

At the date of publishing GridEcon advises a commercial Helium deployer on tokenomics and business strategy. This relationship creates a financial interest in matters affecting Helium's network economics, including HIP 149. GridEcon's editorial standards require independent, source-grounded analysis regardless of this relationship, but readers should weigh this disclosure when evaluating the piece. GridEcon holds no other undisclosed compensation, token allocation, or advisory relationship with Nova Labs, the Helium Foundation, or any entity named in this case study.