GEODNET: Building a Global Coordinate Layer

Imagine, a delivery drone finding the right doorstep, a tractor planting seeds in precise rows, a construction robot working inches from other machinery. None of these work with standard GPS, which is accurate to within 3 to 5 metres. Autonomous systems need centimeter-level precision, and the infrastructure that delivers it underpins a $30 billion global market with adjacent industries totaling $200 billion. (VanEck)

GEODNET is the decentralized network built to serve that market. Launched in December 2021, it coordinates more than 20,000 satellite reference stations across over 150 countries (Dune), delivering Real-Time Kinematic correction data to enterprise customers in agriculture, autonomous vehicles, robotics, and construction. It has surpassed centralized incumbents like Trimble in station count while reducing deployment costs by more than 90% (VanEck).

The network manages tokenomics through a buyback and burn model, directing 80% of dollar-denominated revenues into permanent token destruction. The net deflationary threshold for mining emissions sits at approximately $15M ARR at the current token price of $0.15, dropping to roughly $8.2M after the June 30, 2026 halving cuts mining emissions. The network had already cleared that post-halving threshold, though approximately 80 million tokens in remaining team and investor unlocks will continue adding to circulating supply through late 2026. Grid Econ's model indicates the token is unlikely to meaningfully re-rate until the protocol demonstrates 50% annualized revenue growth and stable earnings multiples over the the next 12 months. This is an opportunity for patient investors with potentially attractive entry points at $0.15 or below between now and year-end. (See price sensitivity tables in Section 8.2)

1.1 At a Glance

1.2 Decentralizing Positioning

GEODNET launched in December 2021, at a moment when DePIN asset prices were near all-time highs and crypto-funded infrastructure projects were starting to attract serious institutional attention. The network was founded by three entrepreneurs with deep roots in navigation technology and blockchain: Mike A. Horton, Yudan Yi, and David Chen. The team had identified a structural bottleneck in creating a global RTK service network as there was no public cryptographically secure network to protect the approximately $1 trillion location aware applications (GEODNET via Navigation Journal). Incumbents like Trimble and Hexagon dominated the space, but their model was capital-intensive, a single RTK base station required between $10,000 and $50,000 to install and maintain, making global coverage economically impractical for any centralized operator to achieve alone. Service coverage from these players is mainly relegated to OECD markets (VanEck).

Observing the crowdsourced infrastructure models pioneered by Helium and Filecoin, the founders saw an opportunity to apply the same logic to precision positioning: replace centralized capital expenditure with a tokenized contributor network. Where Trimble required tens of millions in deployment capital, GEODNET's model required only a $700 miner device purchased by the operator themselves, reducing the cost of network participation by more than 90% and opening global coverage to a permissionless contributor base. (VanEck)

Horton's path to this moment was decades in the making. During his time at UC Berkeley, he began experimenting with MEMS acceleration sensors, the technology that underpins smartphones, automotive airbags, and industrial machinery by converting mechanical motion into electrical signals (PCB Piezotronics). That early work shaped a career spent at the intersection of navigation hardware and autonomous systems, culminating in his co-founding of Crossbow Technology in 1995 (wikipedia) and later, GEODNET itself.

The founding vision did not stop at building a network. In January 2025, while remaining active at GEODNET, Horton and Yi co-founded HYFIX, a U.S.-based company focused on autonomous systems chips for drones and precision positioning hardware, including the miner devices that operate on GEODNET. Horton serves as CEO and Yi as CTO (LinkedIn). HYFIX is both a hardware supplier to the GEODNET ecosystem and a builder of the machines that depend on it, reflecting the founders' longer-term ambition: not just to build the world's most accurate positioning network, but to build the autonomous systems that will run on top of it.

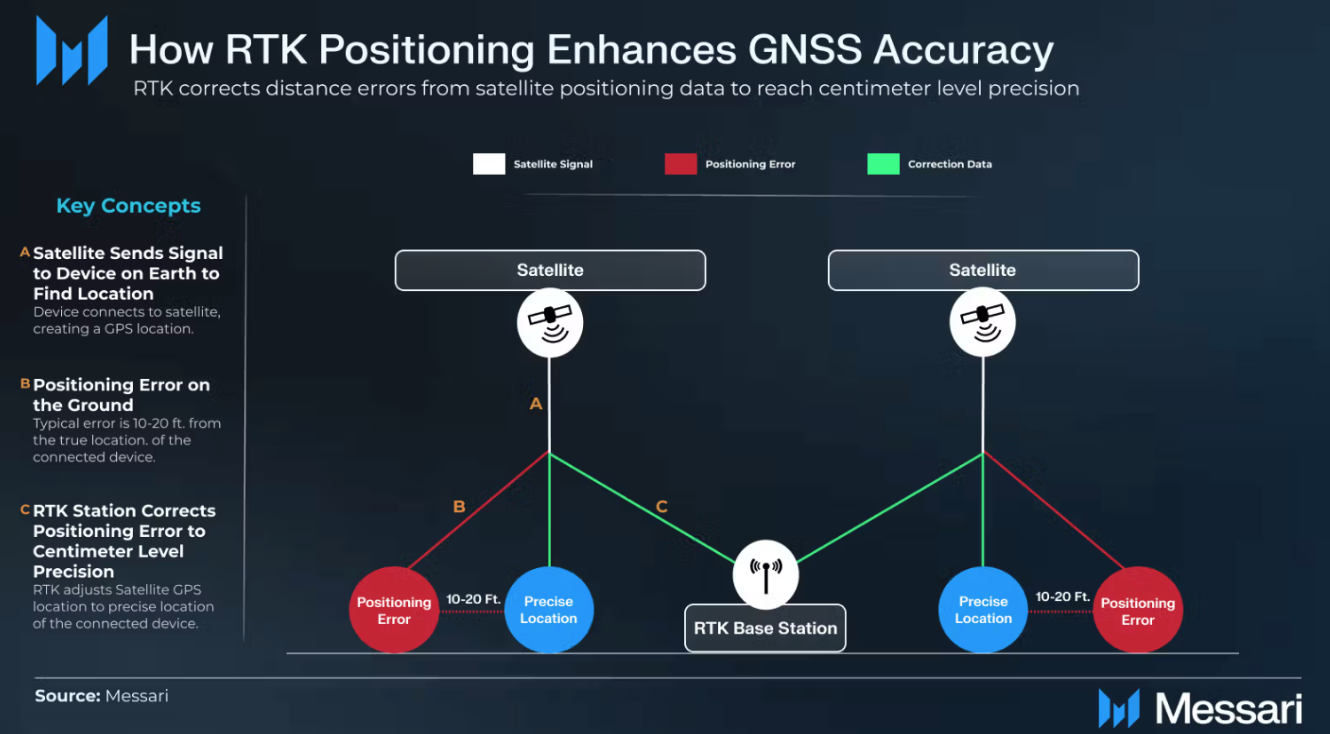

2. From Metres to Centimeters: How RTK Works

Every smartphone, vehicle, and connected device in the world uses satellite signals to determine its location. The satellites themselves are orbiting thousands of miles above the Earth, and by the time their signals reach the ground they have been stretched, bent, and delayed by the atmosphere, introducing errors that make standard GPS accurate only to within 3–5 metres. For most everyday uses, that is close enough. For a drone making an autonomous delivery, a tractor following a precision planting path, or a robot navigating a construction site, it is not.

Real-Time Kinematic positioning, RTK, solves this by placing a network of fixed reference stations on the ground. Each station sits at a location whose exact coordinates are already known to centimeter precision. When that station receives the same satellite signals your phone does, it can immediately calculate how far off those signals are from where they should be, then broadcast those corrections to any device operating nearby. Those corrections achieve positioning accuracy of one to two centimeters. (Wikipedia)

See the following diagram illustration of how RTK enhances GNSS accuracy.

Messari

3. The Stack from Precision to Subscription

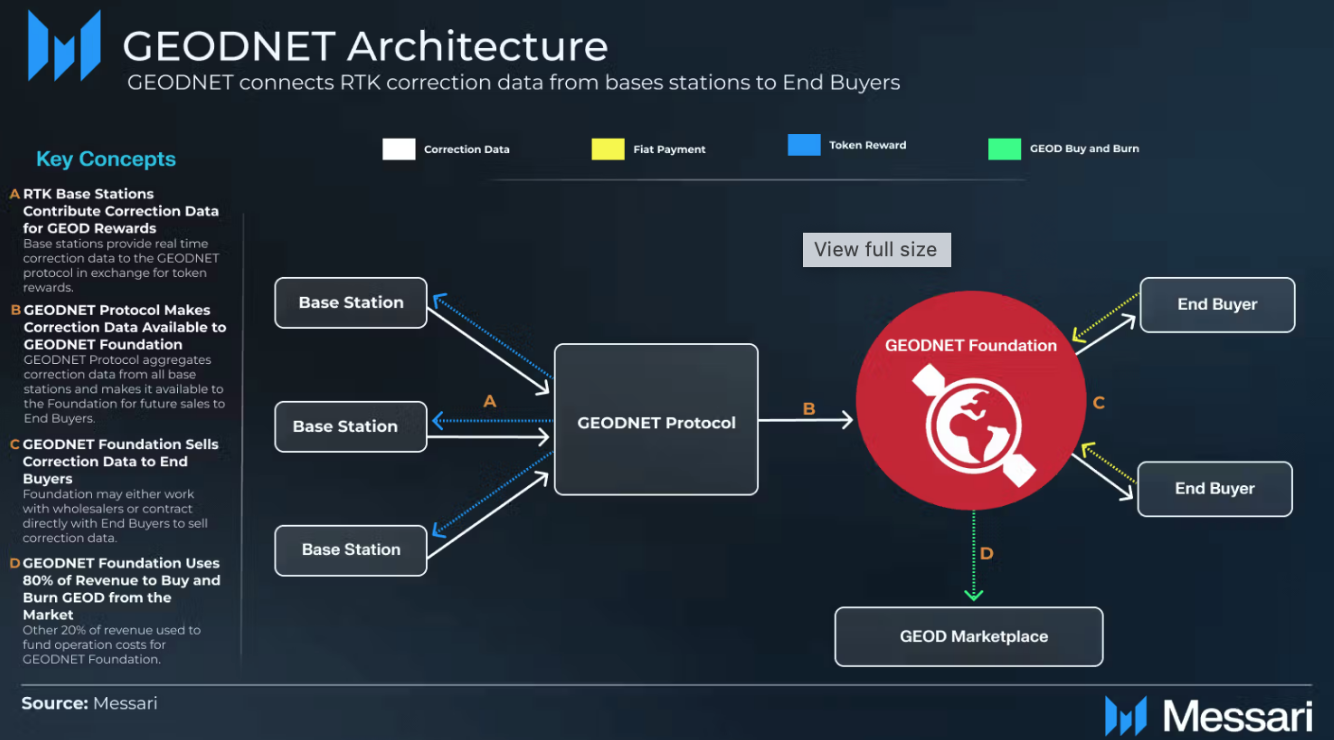

RTK correction data is only as valuable as the infrastructure delivering it. A single base station serves a limited radius, and building a global network of them through traditional centralized means would require billions in capital expenditure. GEODNET solves this by replacing centralized infrastructure investment with a tokenized contributor network. The architecture diagram below shows how: independent operators deploy base stations and contribute correction data to the GEODNET Protocol, which aggregates it and makes it available through the GEODNET Foundation to enterprise end buyers. Those buyers pay in fiat. Eighty percent of that revenue flows back into the open market to buy and burn GEOD tokens, rewarding the contributors who built the network in the first place.

Messari

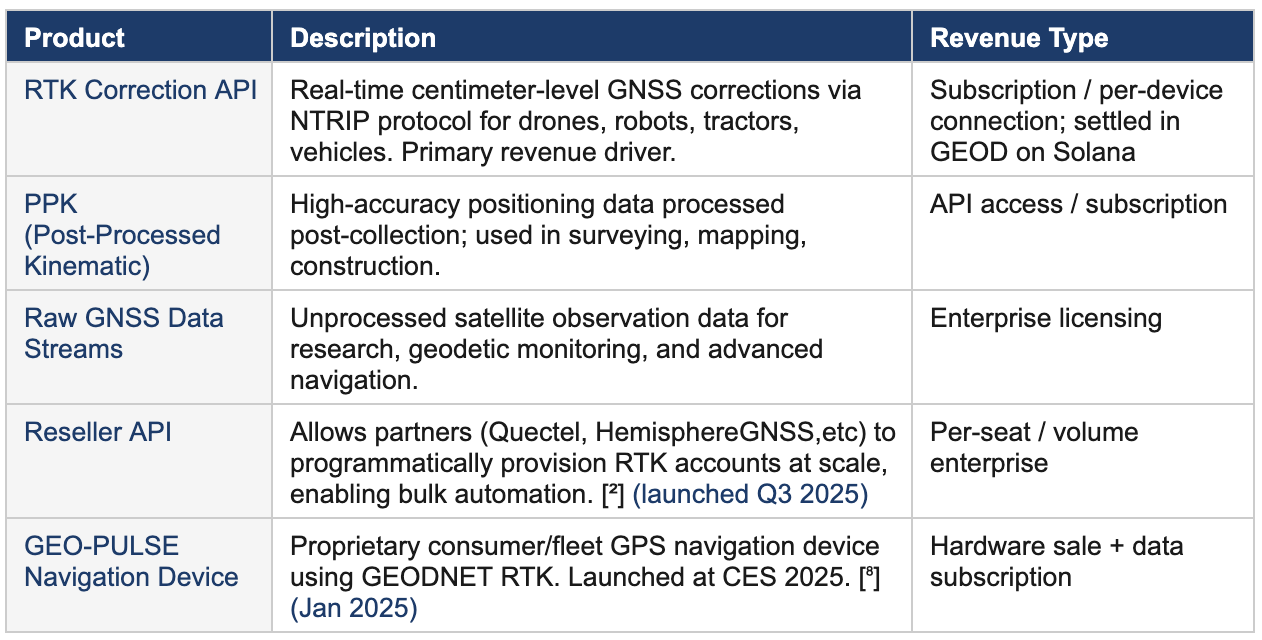

GEODNET's product suite reflects the architecture of a data network. The Foundation's commercial focus is exclusively the sale of RTK correction data, delivered through APIs, subscriptions, and enterprise licensing arrangements. The business model focuses on B2B sales however any consumer can buy RTK services from GEODNET. The hardware ecosystem that makes the network possible, primarily supplied by HYFIX, is a separate business outside of the foundation. The table below catalogs the full product stack, with revenue classification noted for each line item.

RTK Correction API: GEODNET, PPK & RAW GNSS Data: Businesswire, Reseller API & GEO Pulse: Messari

4. Market Opportunity

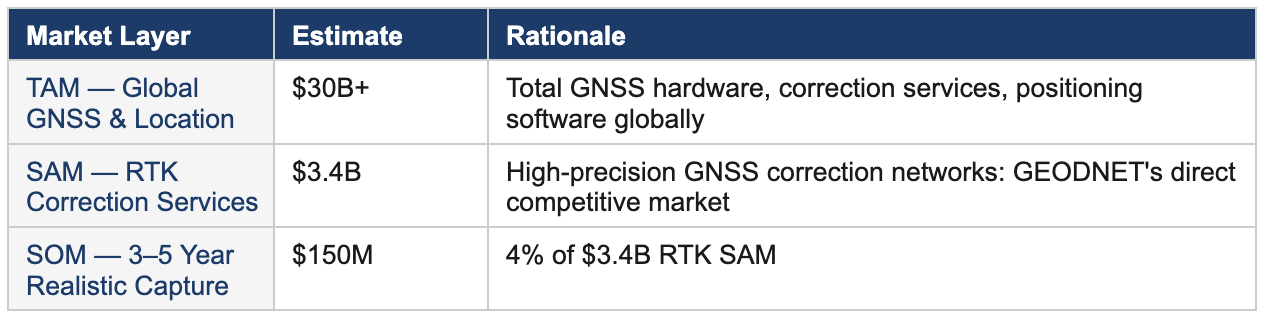

4.1 From Niche to Industry: Sizing the Opportunity

The RTK correction services market sits at an inflection point. Autonomous systems from agricultural robots to delivery drones to self-driving vehicles are quickly moving to commercial deployment. Precision agriculture is transforming how the world feeds itself, with RTK-guided equipment reducing input waste and improving yields across millions of hectares. The market figures below reflect existing, established demand.

These figures do not fully account for the new demand that GEODNET's 90%+ cost reduction makes economically viable for the first time. This is particularly true in emerging markets and among smaller operators who have historically been priced out of precision positioning services entirely. It remains to be seen whether this will be a significant growth avenue for the industry as a whole.

Market sizing: RTK SAM from VanEck

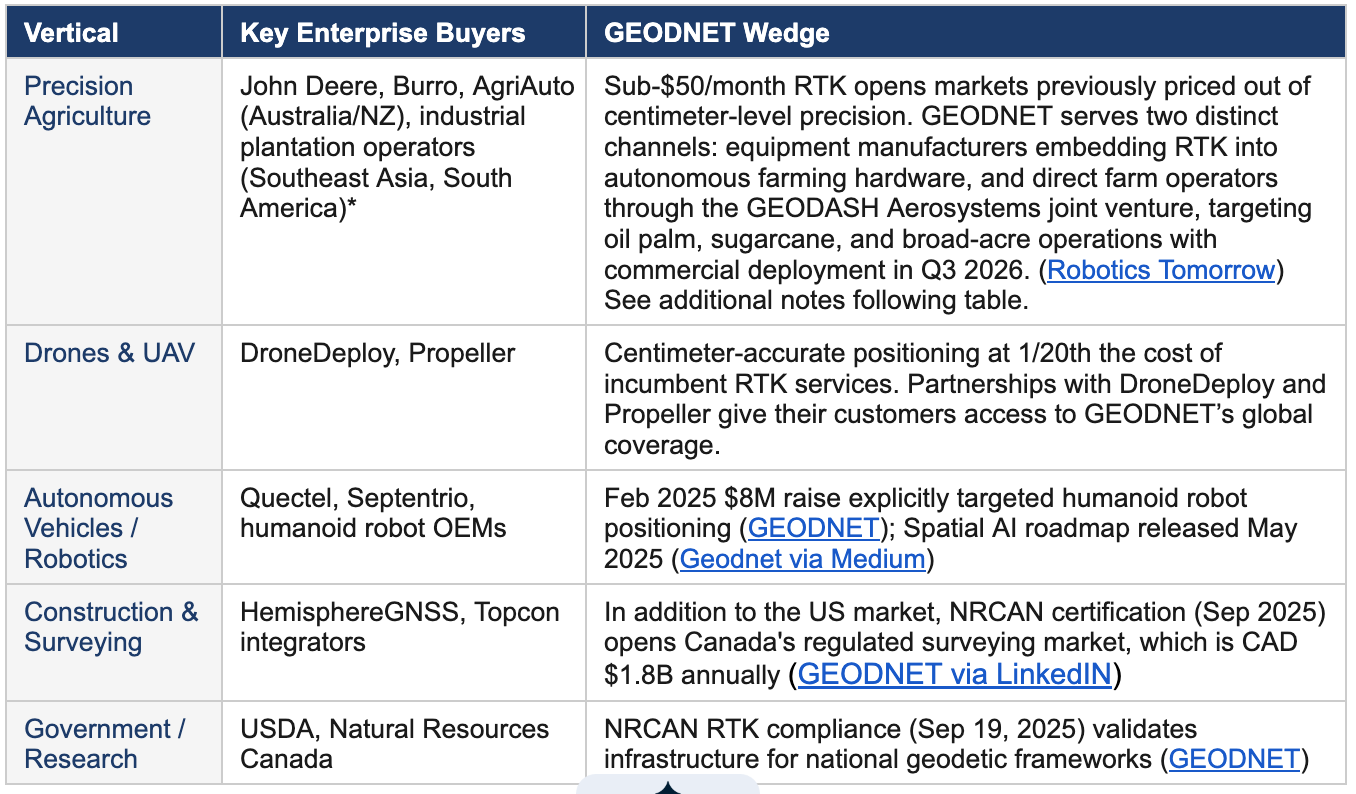

The table above captures the headline market opportunity. The more instructive question for GEODNET's near-term commercial strategy is which segments are accessible first, and why. The following segmentation maps GEODNET's current customer base against the use cases where centimeter-level accuracy creates the clearest, most defensible value. It starts with verticals where commercial relationships are already established and expands toward higher-volume, longer-horizon opportunities in autonomous systems and emerging market agriculture.

4.2 Market Segmentation: Precision has Many Customers

Key enterprise buyers (Inside GNSS), Wedge Sources: Robotics Tomorrow, GEODNET, GEODNET via Medium, GEODNET via LinkedIN, GEODNET

Precision Agriculture: Precision agriculture is a $10B+ global market. Most farms are smallholder operations, which produce about 30% of the world’s food supply (OurWorldinData). The average subsistence farmer in sub-Saharan Africa lives on less than $2/day (UNDP, 2021). Traditional RTK at $500 to +$1,000/year is inaccessible to these farmers. GEODNET's cost model changes the economics. RTK can reach smallholders through shared subscriptions, indirectly through drone service providers, or at scale through NGO and government partnerships.

5. Infrastructure by Incentive

5.1 Verification: Proof of Accuracy Protocol (PoAC)

GEODNET uses Proof of Accuracy Protocol (PoAC). Each base station is continuously scored across: signal quality (SNR ratios), number of tracked satellites, uptime percentage, and physical location integrity. Reward allocation is proportional to score, creating a self-enforcing quality feedback loop, low-quality stations earn less and self-select out economically. (GEODNET)

5.2 From Rooftops to Revenue

GEODNET’s hardware ecosystem is built on a global network of retail partners who sell certified satellite reference stations to contributors worldwide. The stations themselves are primarily manufactured by HYFIX, a related entity co-founded by GEODNET's own Mike Horton, and Rock Robotics. Stations come in dual-band and triple-band configurations and are available to contributors for approximately $700 (GEODNET). Once deployed, station performance is continuously evaluated under GEODNET's Proof of Accuracy Protocol, with underperforming stations receiving reduced rewards (GEODNET).

Following the June 2026 halving, dual-band miners will earn 6 GEOD per day. At a GEOD price of $0.15, that translates to approximately $0.90 per day or $328 per year, implying a hardware payback period of around 2 years. At that return rate, continued operator participation depends meaningfully on token price appreciation. The relationship is self-reinforcing in both directions: a rising GEOD price shortens payback periods and strengthens retention, while sustained operator participation maintains the coverage quality that drives enterprise demand and supports the buyback-and-burn mechanism that underpins token value. With GEODNET’s network of +20k miners the focus is more on network quality and retention vs. coverage growth.

The current hardware model relies on proprietary designs, which limits third-party manufacturing risk but constrains the speed at which the network can scale. As GEODNET matures, a transition toward standardized third-party hardware would support faster deployment without compromising the quality standards the protocol depends on.

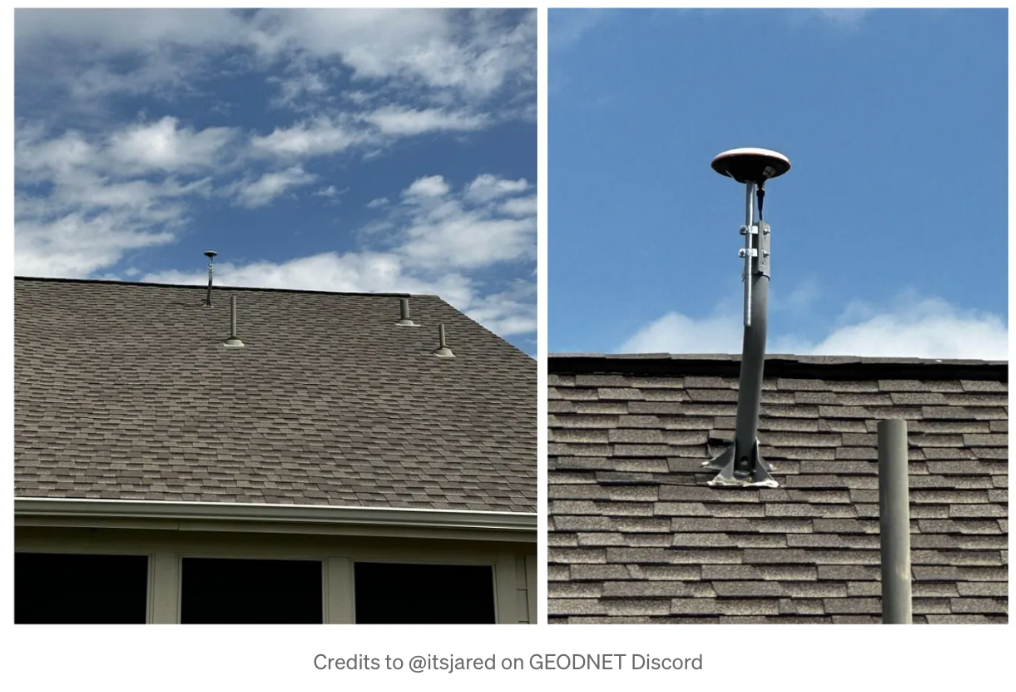

See the below photos for an example of a GEODNET compliant reference station.

(via Borderless Capital)

5.3 Build it and They will Earn

Getting started as a GEODNET supplier comes down to finding the right location. The network divides the world into geographic hexes, and the first operator to get a station running at 98% or better Rolling Reward Rate for 30 consecutive days in a given hex earns a Location NFT. That NFT is essentially a first-mover certificate, it protects the operator from having future stations eat into their rewards. Recently, GIP-8 added a retention requirement in November 2025. Operators now need to maintain at least 80% RRR to keep their NFT. Drop below that and it moves to whoever is performing best in the hex. The network is still open to new stations beyond the 20,000 NFT cap set under GIP-7, though latecomers earn at a lower rate and without the first-mover protections.

Picking the right location matters just as much as deciding to participate. The SuperHex staking program is how GEODNET solves this. Token holders stake GEOD into specific hexes that enterprise customers have identified as high-value, and stations that deploy into those active hexes earn up to four times the standard reward rate. The result is a system that points hardware toward the places where demand already exists, and rewards operators who keep their stations running well rather than just those who show up first. (GEODNET)

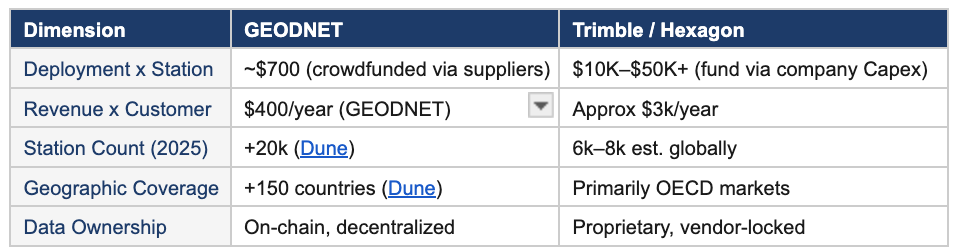

6. Competitive Landscape

6.1 Challenging the Establishment

The differentiating factors between GEODNET and its centralized competitors are price and network as the RTK signal is the same among all market players. Beyond the hardware cost differential, GEODNET and its incumbents operate fundamentally different business models to capture customers.

Trimble and Hexagon are vertically integrated hardware and software companies. They manufacture proprietary receivers, sell correction network subscriptions, and embed RTK services into multi-year enterprise contracts with surveyors, construction firms, and agricultural equipment manufacturers. This revenue model depends on high margins from proprietary hardware and captive subscription relationships. This structure supports sticky recurring revenue but limits geographic reach to markets where the economics of centralized station deployment are favorable: typically high-income, high-density regions.

Concurrently, GEODNET operates as a data marketplace rather than a hardware company. Customers access RTK correction data via API without purchasing proprietary hardware. This model prioritizes network scale and geographic reach, producing a structurally lower cost base and the ability to serve markets that incumbents cannot profitably reach. The trade-off is that GEODNET's revenue is entirely dependent on the growth of its data subscription base. GEODNET has a 90% cost advantage, therefore the probability of a competitor building global network with a cost advantage over GEODNET is low.

See the below table for summary for the differences between GEODNET and its incumbents.

Incumbent station counts and pricing are industry estimates; no public Trimble network count is available. Cost differential from Borderless Capital and VanEck

7 The Token that Funds the Network

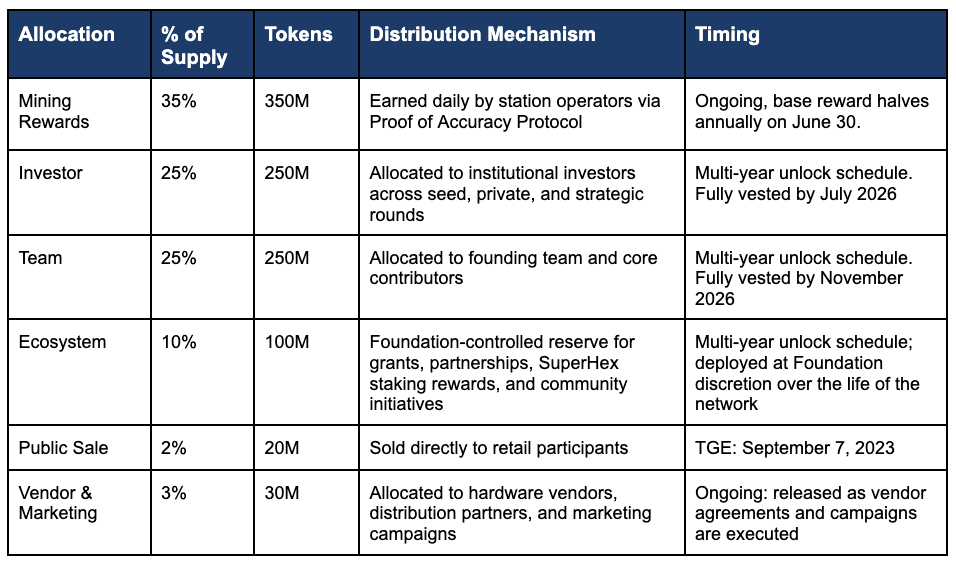

7.1 Counting to One Billion

GEOD has a fixed total supply of one billion tokens, distributed across six allocation categories designed to balance network growth, contributor incentives, and long-term protocol sustainability. The largest share goes directly to station operators through ongoing mining rewards. Base reward rates halve annually every June 30 to manage emissions over time. Institutional investors and the founding team each hold 25%, both following multi-year vesting schedules that complete by late 2026. The remaining 15% is split across an ecosystem reserve under Foundation control, a public sale at token generation in September 2023, and ongoing vendor and marketing allocations. Together, the schedule reflects a protocol that front-loaded its supply distribution to bootstrap the network, with the most consequential dilution events now firmly in the rearview mirror.

(GEODNET)

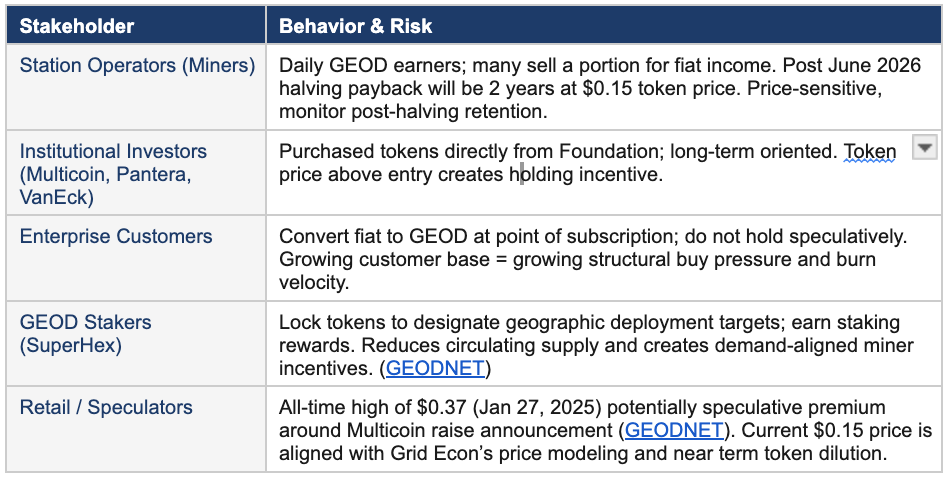

7.2 The Players Behind the Tokens

Token markets are shaped by the behavior of the participants who hold and transact within them. GEOD is no different, and understanding who owns the token, why they hold it, and under what conditions they sell is as important as understanding the supply schedule itself. Five distinct stakeholder groups interact with GEOD, each with different economic incentives, time horizons, and thresholds for selling. Station operators earn daily and sell to cover operating costs. Institutional investors hold against a known cost basis with vesting-driven liquidity windows. Enterprise customers convert fiat to GEOD at the point of subscription, creating recurring structural buy pressure without speculative intent. Stakers lock tokens to direct network deployment, removing supply from circulation. Retail participants respond to narrative and momentum. The interplay between these groups, rather than any single factor, determines how token price behaves in practice.

7.3 Buyback-and-Burn Mechanism: Revenue In; Tokens Out

GEODNET routes 80% of all protocol revenue into open market purchases of GEOD on Solana DEXes, with every purchased token permanently destroyed and the remaining 20% retained by the Foundation for operations. Burned tokens are irreversibly removed from circulating supply with no recycling to reward pools, making each burn a permanent reduction in total tokens outstanding. (GEODNET).

Because mining emissions are fixed in tokens and the buyback operates in dollars, the net deflationary threshold moves in direct proportion to token price. A 20% price increase requires a 20% revenue increase to hold the same deflationary position. At the current price of approximately $0.15, the network needs roughly $15M in ARR to offset today's mining reward rate. The June 30, 2026 halving cuts mining emissions by 50%, dropping that threshold to approximately $8.2M ARR at the same price. Strong April and May revenue numbers point to an ARR of $9.4M. Should GEOD re-rate to $0.20 post-halving, the threshold rises to approximately $11M, meaning revenue growth must keep pace with any price appreciation to sustain net deflationary status. The mechanism is self-reinforcing in both directions, and discounting large price swings, the halving is the most consequential near-term catalyst for tipping the balance.

8 Measuring the Opportunity

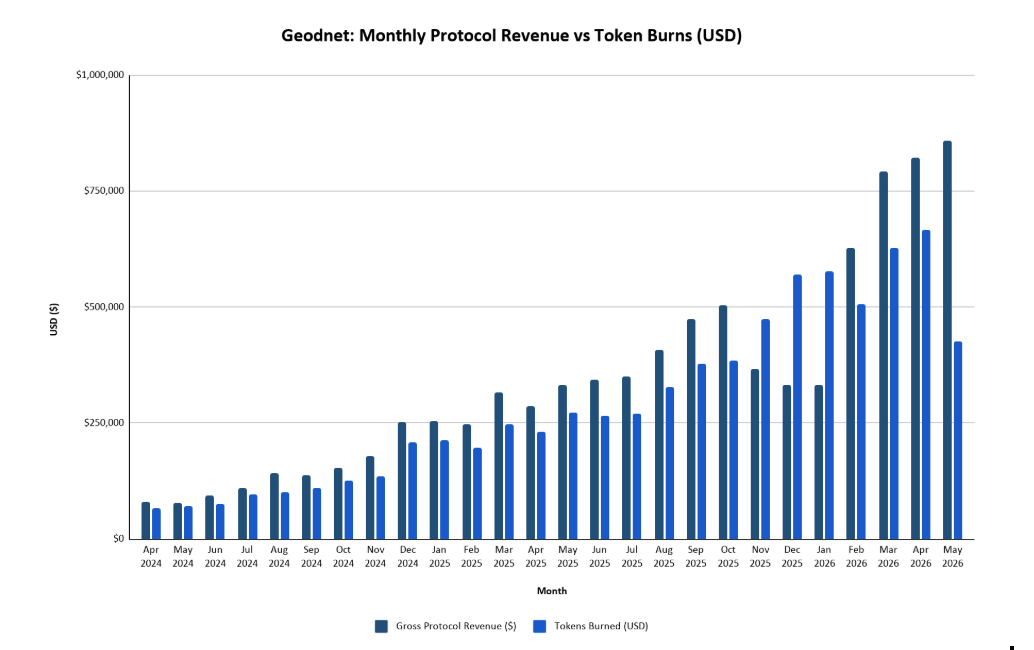

8.1 The Revenue Behind the Burns

Revenue quality is high: the primary stream is recurring enterprise subscriptions, not one-time transactions. Customers include Quectel, DroneDeploy, Propeller, USDA, HemisphereGNSS, and Septentrio (Inside GNSS). The reseller API model launched in Q3 2025 turns OEM partners into revenue multipliers, with each partner activating its downstream install base without requiring direct GEODNET sales effort. (Messari)

The following chart shows a clear upward revenue trend since April 2024, with some monthly variation. Early 2026 performance indicates that GEODNET has reached an annualized income of approximately $9.4M

Revenue from Defi Llama, Token burns from Dune

From November 2025 GEOD's price had dropped significantly from its early 2025 highs of ~$0.30 down to around $0.15. This means each dollar of buyback capital is purchasing far more tokens than it would have earlier in the year which can make the burn look outsized relative to revenue when valued in USD. Additionally, if GEODNET batches its burns rather than executing them continuously, any given month could reflect buyback capital accumulated over several prior months, further inflating a single month's burn figure beyond that month's revenue alone.

8.2 The Multiple Behind the Token

Given that 80M tokens will be unlocked to investors and team members before the end of the year Grid Econ sees price appreciation coming from multiple expansion and/or revenue increases. The current market price takes into account the 80M in token unlocks occurring over the next 12 months at conservative revenue growth. See the following sensitivity tables for pricing under different revenue and multiple scenarios over the next 6 - 12 months.

P = Revenue × (Multiple + 0.80 × Years) / Gross SupplyNet Supply = Gross Supply × Multiple / (Multiple + 0.80 × Years)Gross supply: 533.5M (6mo) | 546.7M (12mo) | Starting float: 438M (CoinGecko) + remaining investor vest (10.8M) + remaining team vest (68.8M) + post-halving mining emissions.

Due to crypto market multiple instability, Grid Econ recommends performing this analysis at the end of year to get a clearer picture of 2027 valuation levels. However if an investor has a +12 month timeline horizon they should look for entry points at or below $0.15 especially as revenue growth continues.

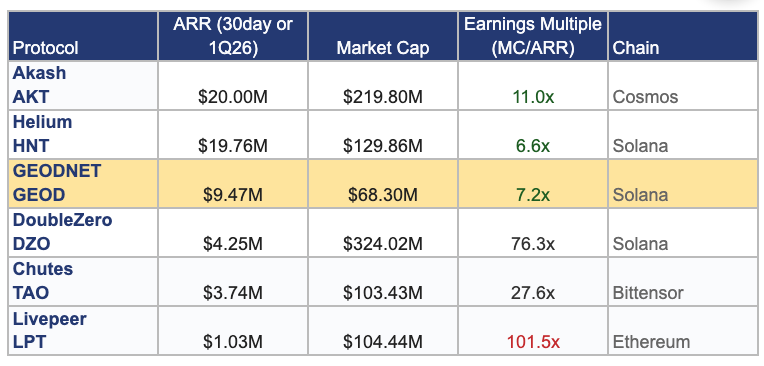

8.3 DePIN Peer Valuation Comparison: How GEODNET Stacks Up

GEODNET continues to gain traction among its DePIN peers with respect to revenue generation. Market multiples still vary widely. Even with current market conditions, GEODNET has proven itself as an established player in the space. The network scores favorably with respect to revenue generation and appears to have room for multiple expansion. See the following table:

Sources: Revenues Token Terminal, Defi Llama or protocol statements, Market Cap from Coingecko.

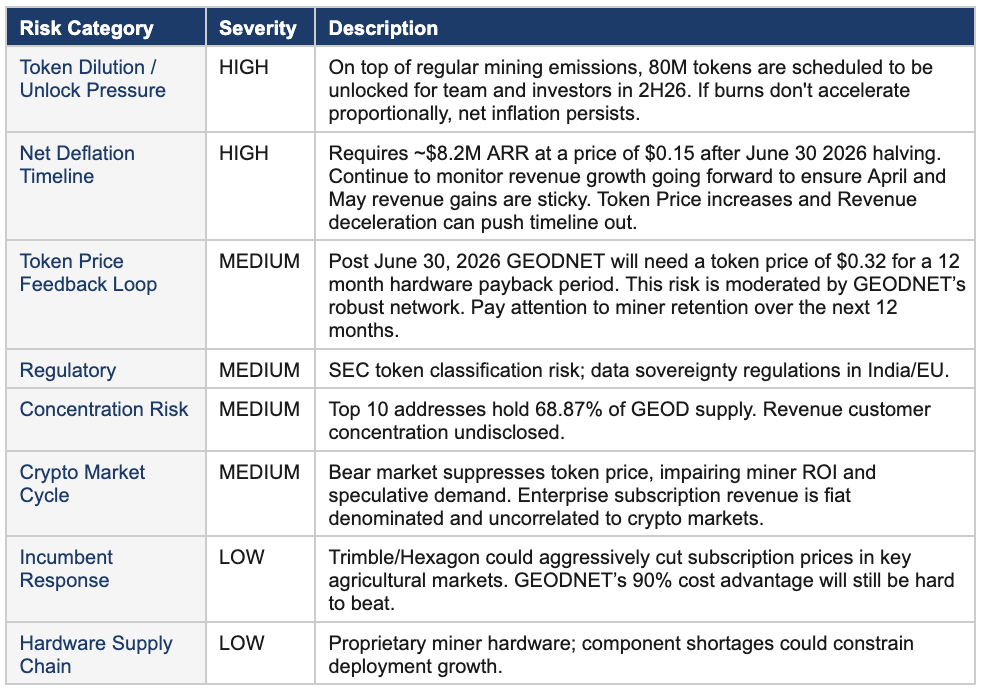

9 Risk Matrix: Signals to Watch

Most crypto risk matrices lead with regulation, market cycles, and competition. GEODNET's near-term risks sit elsewhere. The dominant exposures are internal to the token itself. Roughly 80M tokens remain scheduled to unlock for team and investors through 2H26, and the June 2026 halving will cut mining emissions in half. The interaction between unlock pressure, post-halving emissions, and the pace of enterprise revenue growth determines whether the network reaches net deflation on the timeline modeled here, or whether that milestone slips into 2027. Regulatory classification, market cycles, and incumbent response remain on the matrix but rank lower because none of them are positioned to alter that timeline the way the supply-side mechanics can. The table below ranks each risk by severity.

GEODNET has built a network with real enterprise customers paying in fiat for a service the existing industry already buys. The 20,000-station footprint is real, the revenue is recurring, and the buyback mechanism converts that revenue into permanent token destruction without recycling. What the market is pricing today is not the network itself but the overhang. Eighty million tokens remain to clear, and the June 2026 halving has not yet reshaped the emission math. Both resolve within twelve months. Investors with that horizon are being offered a known asset at a price set by known dilution, with revenue growth as the variable that determines the re-rate. The work from here is watching whether enterprise adoption keeps pace with the supply schedule, and whether the post-halving operator economics hold without requiring token price to do the work.